Infra Play #144: Dell

With the recent focus on the infrastructure part of cloud infrastructure software, it's appropriate to take a look at some of the hardware + software plays in the industry. I've previously covered NVIDIA and Oracle, but I think that it's time to take a look at a company that has been making headlines with its rapid expansion of its AI server business.

The key takeaway

For tech sales and industry operators: Dell is a stable, slow-moving organization that rewards a specific kind of operator: one who delivers outcomes without needing the company to move fast. Realistically speaking, its headline growth is tied directly to repackaging NVIDIA hardware and installing it for customers, while keeping a small portion as margin for itself. The work itself is hard (rack-scale integration, liquid cooling, power delivery, and on-site deployment at speed are genuinely difficult), but only the select few driving the largest customers will benefit from this turnaround. The window for individuals to join the business and benefit is likely over (unless you want to grind the next regular server replacement cycle), similar to the Oracle OCI opportunity in 2025.

For investors and founders: On paper, Dell is a fair business at a fair price, albeit not a wonderful one, to borrow Buffett's framing. It has built a world-class supply chain and proven it can reprice and reroute under stress, and that is not nothing. But value flows to whoever solves the hardest physics, and here that is the chip and the memory, not the chassis around them. For founders, the lesson is to own the bottleneck, not the assembly. If your company's role can be described as integrating someone else's breakthrough, your margin will always be set by someone else's scarcity. For investors, Dell is the lower-risk seat in AI infrastructure: no foundry or CapEx exposure, a cheap valuation, and management beholden to shareholders, with a capped margin as the price of that safety. Personally, I think there are better uses of capital at this stage of the buildout.

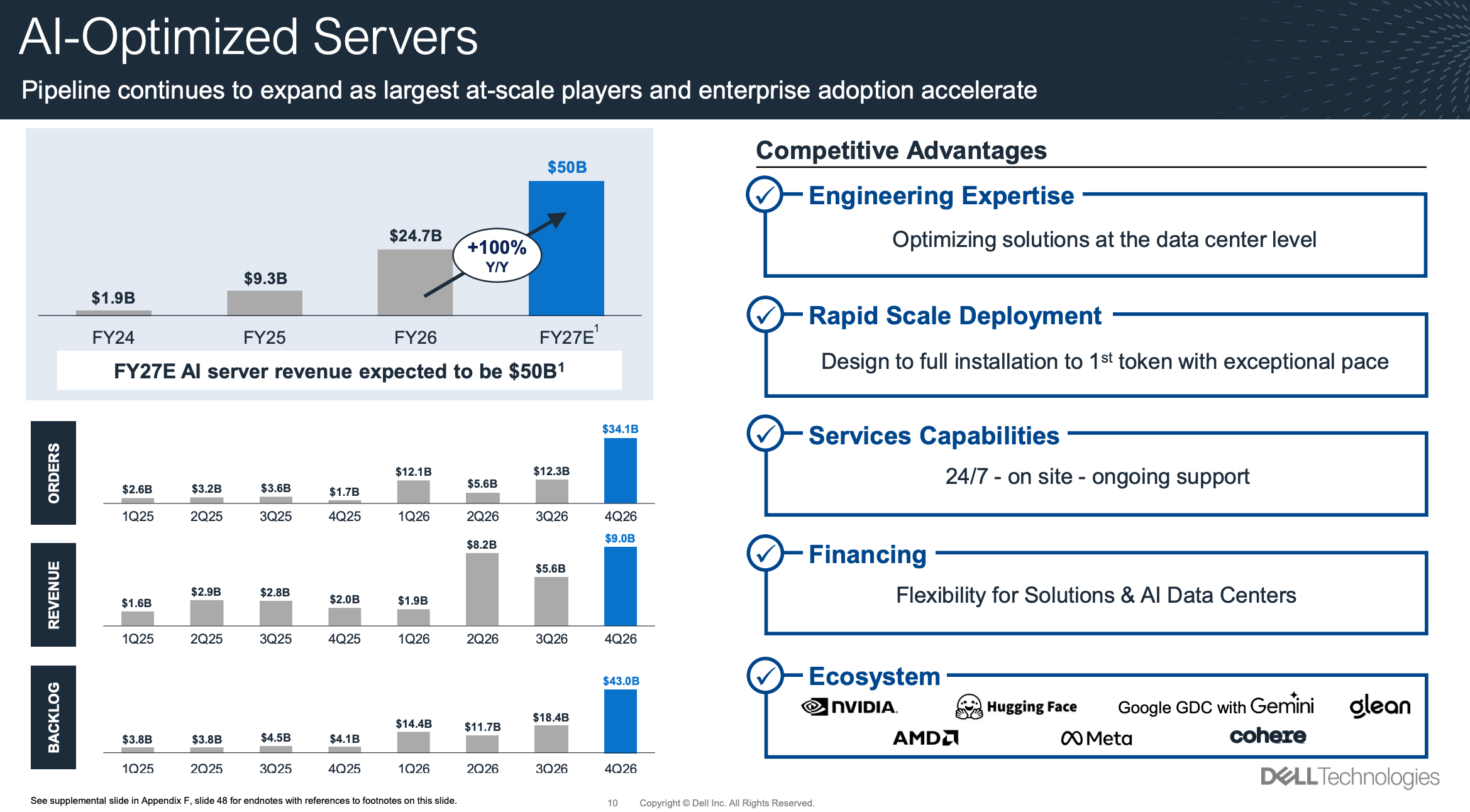

The sleeping giant

Jeff Clarke: FY26 was a defining year in our company's history. We delivered record full year revenue and EPS. Revenue reached $113.5 billion, up 19% and EPS grew 27% to $10.30. We converted that performance into a record annual cash flow over $11 billion and returned $7.5 billion to shareholders, including 54 million shares repurchased more than doubled last year. The AI opportunity is meaningfully growing and transforming the company. In FY26, we closed $64.1 billion in AI orders shipped $25.2 billion and exited with a record $43 billion in AI backlog. Powerful proof points that our engineering leadership and differentiated solutions are winning.

We are executing with discipline and speed. We are gaining share in our PC business and strengthening ISG with strong margins in traditional servers and storage, all while positioning the company for the AI era. It was a monumental year. We exit with strong momentum, and I couldn't be more proud of this team. With that, let me turn to the key highlights for the quarter. We delivered a record quarter. Q4 revenue was $33.4 billion, up 39% and earnings per share was $3.89, up 45%, driven by disciplined execution and demand for our AI solutions. While operating in a dynamic environment, we saw a record cash flow generation and above trend capital returns for shareholders.

Now let's move to AI. We kept an already strong year with an exceptional quarter for AI, record orders and broad-based demand. In Q4, we booked $34.1 billion in AI orders, evidence that demand is accelerating as customers deploy AI at scale. We shipped $9.5 billion in AI servers in the quarter. We exited Q4 with a record $43 billion in AI backlog, and our pipeline continued to grow sequentially even after converting $34.1 billion of orders, a clear sign of sustained momentum. For the full year, AI orders reached $64.1 billion. Our customer base surpassed 4,000 with growth across neoclouds, sovereigns and enterprise customers, evidence that demand is broadening across all customer types.

We're winning for the reasons we've outlined all year. Engineering for performance and time to market while optimizing TCO for AI workloads, deployment and installation at speed and scale, ongoing life cycle support that keeps clusters up and running and DFS financing. We're doing this with discipline. Profitability is in line with our mid-single-digit operating margin target. We like our position, the line of sight we have with our backlog and pipeline and the advantage our scale and supply chain bring.

An AI server is a high-performance system built specifically for artificial intelligence work. Unlike regular servers that handle a wide range of tasks, Dell's PowerEdge XE series is designed from the ground up with GPUs in mind. It prioritizes high GPU density, fast connections between the accelerators, strong power delivery, and advanced cooling, including liquid cooling for the densest setups. This makes the servers well suited for both training large models and running inference at scale.

The AI server business line now generates $50B annually, after another exceptional year by the team.