Infra Play #130: Palantir revisited

Software that dominates...earnings?

There are some things in life that are inevitable, such as death, taxes and Palantir being controversial. I last wrote about them 14 months ago and made the following directional predictions:

For tech sales: Palantir has an exceptional product and deep domain expertise in driving LLM and Enterprise-grade ML adoption within customers with large scale projects. It’s also a company that deeply despises sales reps. Avoid at all costs until a structural change at leadership level.

For investors: I’ll not speculate on where the price of the stock will go because all bets are off when we are talking about a “darling” of the retail community. From a purely product and customer integration perspective, the company is one of the 3 strongest players in AI adoption today. The continued mismanagement of the GTM team raises significant questions around how sustainable growth is on a long enough time scale.

As far as directional bets go, this was quite accurate. Working in GTM there remained a poor experience, but the technical knowledge and strong culture drove significant company growth, including 110% stock price gains.

With this out of the way, let's try to assess where Palantir sits today, at a time when the data+AI layer has never been seen as more important, yet somehow it appears that a lot of the growth is happening in other companies.

The key takeaway

For tech sales and industry operators: I've never understood companies that treat distribution as a cost to be minimized rather than a capability to be compounded. Palantir has built an extraordinary product and then deliberately underinvested in the people who bring it to market, which works when demand exceeds supply but creates fragility the moment competition catches up. They're leaving enormous value on the table by treating sales as philosophically beneath them rather than engineering a distribution system that matches the quality of their product. In a world where Databricks is aggressively capturing the Data+AI market, while still being very picky about who they hire (“will this individual help us improve faster than our current team”), the reality is that Palantir has reached this level of growth while trying to actively deprioritize its commercial efforts, not because of some “lone wolf” genius approach to the market.

For investors and founders: Palantir at a Rule of 40 score above 90 is the best financial profile in enterprise software today. The question is whether this is the beginning of a new era or the high water mark. The $10B Army deal and $448M ShipOS contract are framework ceilings, not committed revenue, and the same mechanic that made Salesforce's $5.6B announcement misleading applies here with even higher stakes. International revenue is stagnating while 73% concentration sits in the US, creating single point of failure exposure to political cycles and defense budget sequestration. The technology moat is the ontology layer and process mining capabilities, but it's eroding as LLMs become increasingly capable of analyzing operational data and generating automation code without a proprietary platform. At current multiples you're paying for a decade of compounding at rates that assume perfection across government retention, international expansion, and continued technological superiority. The harsh reality is that software line items within defense budgets are among the first to face scrutiny during consolidation phases because they lack the constituency protection that hardware programs enjoy. We've reached peak Palantir.

The American company in a multipolar world

Alexander C. Karp: We are at the outset, the very beginning, of a generational project.

Our financial results, those crude and imperfect metrics by which a market filled with both excitement and fear attempts to assess the value of the companies it covets, have again exceeded even our most ambitious expectations.

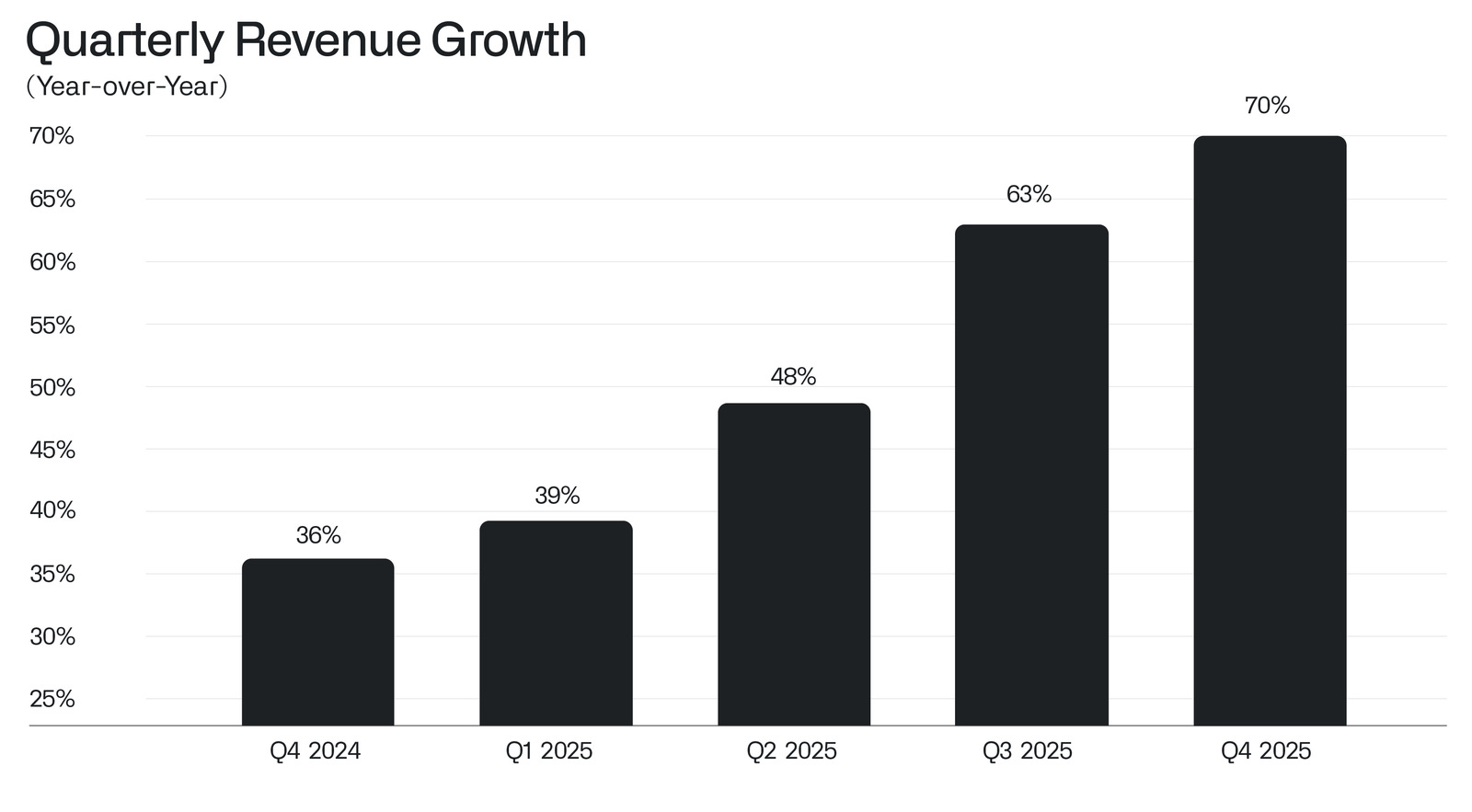

We generated $1.4 billion in revenue in the fourth quarter last year, a new record in our twenty-three year history—representing a 70% growth rate over the same period the year before.

Such a massive acceleration in growth, for a company of this scale and size, is a remarkable achievement—a cosmic reward of sorts to those who were interested in advancing our admittedly idiosyncratic project and embraced, or at least did not wholly reject, our mode of working.

The more familiar path for technology companies has been to seek the affection and capital of the public markets, and to monetize at the height of expectation, before entering a long yet certain contraction into obscurity.

We declined to take this approach. Our public offering more than five years ago marked the beginning of our ascent, not its peak.

For a company that hates sales reps, the execution in terms of winning new business has been exceptional.

Alexander C. Karp: And yet we have achieved this level of growth with significant discipline, which is seemingly scarce in the industry today, generating a new record of $609 million of profit in a single quarter, representing a 28% quarter-over-quarter increase.

We still remember, and will not soon forget, enduring for years polite yet firm questions about the potential profitability and indeed more fundamentally the wisdom of our approach.

Other pockets of what some not incorrectly describe as an exuberant market for artificial intelligence systems may feel pressure to manage their businesses around their financials.

Our record profit, however, is pure and uncontrived.

And it is, perhaps more important, the consequence of a business built around software platforms, not legions of well-credentialed consultants with their presentations and wise counsel.

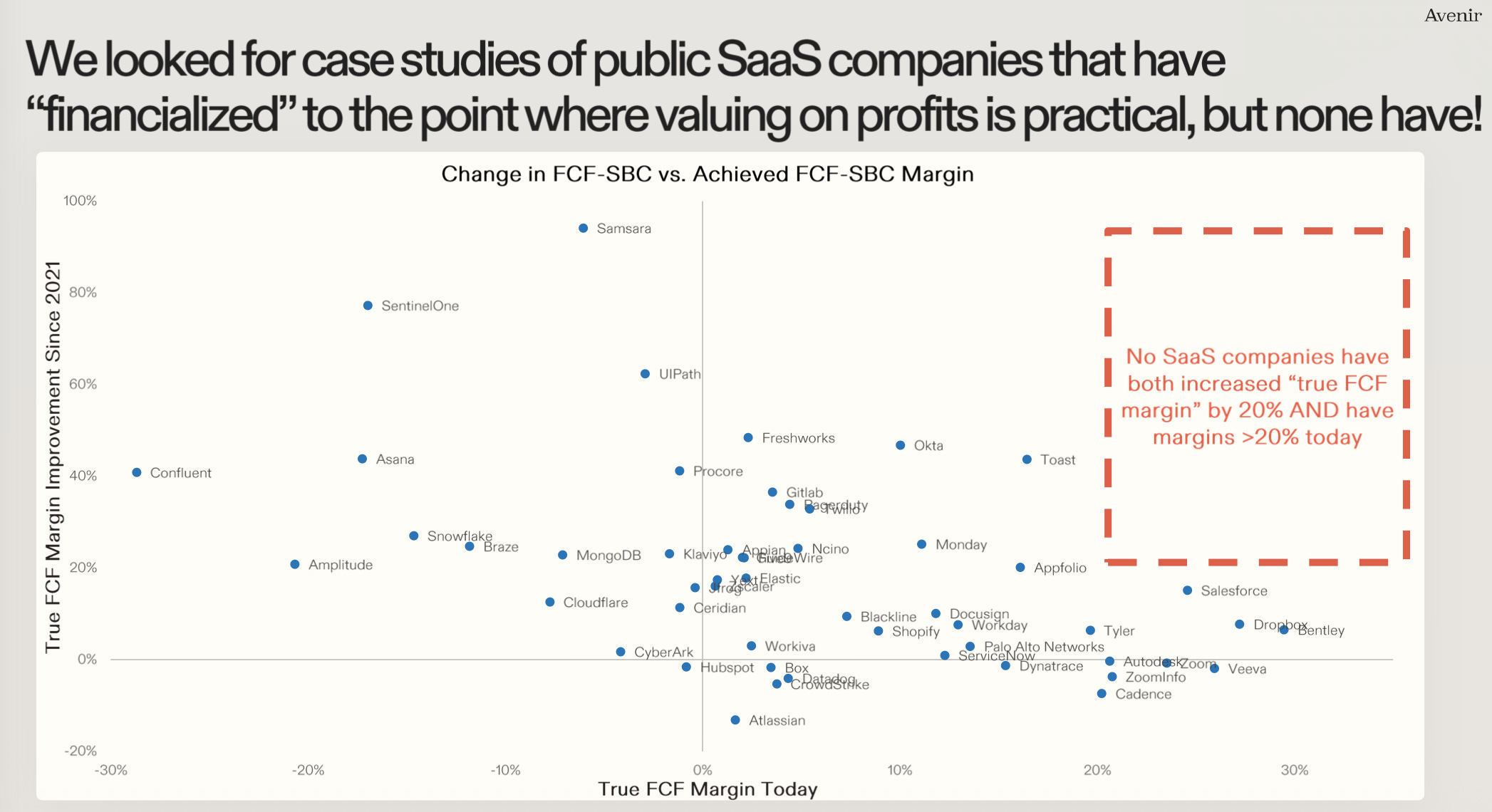

In my “Is SaaS dead?” deep dive, I covered this deeply concerning chart. As I explained:

If you look at the actual profitability of SaaS companies, most are barely at break-even. They might be "performatively" meeting the Rule of 40, but in practical terms stock-based compensation (among other expenses) is killing GAAP profitability metrics.

Infra Play #128: Is SaaS dead?

At the end of last week's deep dive on Salesforce, I added this quote from an experienced investor on the personal impact when a "sector dies":

Now the interesting thing is that if we run the numbers, right now Palantir would actually land very comfortably in the middle of that big empty quadrant. 14 months ago, neither the growth nor the financials were particularly impressive. If the big question was "can Palantir leverage AI to win," I think the answer is very clearly yes.

Why is that?